Hedge funds and private equity are two of the most prominent alternative investment vehicles in global finance. Together they manage trillions of dollars in capital, attract the world's most sophisticated investors, and shape the trajectory of companies and markets alike. Yet they operate in fundamentally different ways, targeting different opportunities with distinct structures, strategies, and time horizons.

Understanding the distinction between hedge funds and private equity is essential for any investor considering an allocation to alternatives. This guide provides a comprehensive comparison across seven key dimensions, from investment structure and liquidity to fees and risk profiles, so you can determine which vehicle best aligns with your financial objectives.

Hedge funds are pooled investment vehicles that trade liquid securities across public markets using flexible strategies, while private equity funds acquire ownership stakes in private companies to create value over multi-year holding periods. This core distinction drives every difference in structure, liquidity, fees, and return profiles between the two vehicles.

A hedge fund is a pooled investment vehicle, typically structured as a limited partnership, that employs a wide range of strategies across public markets. Hedge funds trade equities, fixed income, currencies, commodities, and derivatives, using tools such as short selling, leverage, and quantitative models to generate returns. According to HFR, global hedge fund industry capital surpassed the historic $5 trillion milestone in 2025.

Private equity refers to investment funds that acquire ownership stakes in private companies or take public companies private. PE firms create value through operational improvements, strategic repositioning, and financial engineering over multi-year holding periods. Preqin's 2025 Global Private Equity Report estimates total global PE assets under management at approximately $8.2 trillion.

The table below summarises the fundamental differences between these two alternative investment vehicles.

| Feature | Hedge Fund | Private Equity |

|---|---|---|

| Primary market | Public markets (equities, bonds, derivatives) | Private markets (direct company ownership) |

| Ownership | Minority positions in publicly traded securities | Controlling or significant stakes in private companies |

| Strategy | Trading, hedging, arbitrage, macro positioning | Buyouts, growth equity, operational transformation |

| Liquidity | Monthly or quarterly redemptions with lock-ups | Illiquid; capital locked for 7–12 years |

| Investor base | Accredited investors, institutions, family offices | Institutional investors, sovereign wealth funds, UHNWIs |

| Regulatory framework | SEC Regulation D; limited disclosure (Form ADV, Form PF) | SEC Regulation D; additional SEC and ILPA guidelines |

| Industry AUM (2025) | $5.0+ trillion (HFR) | $8.2 trillion (Preqin) |

While both vehicles serve as alternative investments and share certain structural similarities, the comparison above reveals that hedge funds and private equity operate in fundamentally different arenas. Hedge funds focus on generating returns through trading and risk management in liquid markets, while private equity creates value by transforming businesses over extended periods.

While the overview above captures the broad strokes, the differences between hedge funds and private equity run much deeper. Below are the seven most important distinctions every investor should understand before allocating capital to either vehicle.

Hedge funds are typically structured as open-ended limited partnerships. Investors can subscribe and redeem on a rolling basis, subject to notice periods and lock-up provisions. The fund operates continuously, with capital flowing in and out while the manager deploys strategies across liquid markets.

Private equity funds are closed-end vehicles with a defined fund life, usually 10 to 12 years. Investors commit capital upfront, which is drawn down over a 3- to 5-year investment period as the GP identifies and executes deals. Distributions flow back to investors as portfolio companies are sold or taken public during the harvest period. Once the fund is fully liquidated, it ceases to exist.

Hedge funds employ a diverse range of trading and risk management strategies across public markets. Common approaches include:

Private equity takes a fundamentally different approach. Rather than trading securities, PE firms acquire companies and work to increase their value over several years. Core strategies include leveraged buyouts (LBOs), growth equity investments, and operational turnarounds. The PE manager acts as an active owner, driving strategic changes, improving management, optimising capital structures, and positioning the company for a profitable exit.

Time horizon is one of the starkest contrasts between hedge funds and private equity, and it shapes virtually every other aspect of how each vehicle operates.

| Dimension | Hedge Fund | Private Equity |

|---|---|---|

| Typical holding period | Days to months (trade-dependent) | 4 to 7 years per investment |

| Fund life | Open-ended (perpetual) | 10–12 years (closed-end) |

| Capital commitment | Invested immediately upon subscription | Drawn down over 3–5 years as deals are executed |

Hedge fund managers make rapid decisions, adjusting positions daily or weekly in response to market conditions. Private equity managers take a patient, long-term approach, spending years developing a company before realising a return through a sale or IPO. This difference in time horizon has profound implications for how each vehicle generates returns and how investors should think about portfolio allocation.

Hedge funds offer periodic liquidity, with most funds allowing monthly or quarterly redemptions subject to 30- to 90-day notice periods. Many funds impose initial lock-up periods of 12 to 24 months, and gate provisions may restrict withdrawals during periods of market stress. Despite these constraints, hedge fund capital is significantly more accessible than private equity.

Private equity is fundamentally illiquid. Once capital is committed, investors cannot withdraw it during the fund's life. Distributions occur only when the GP exits portfolio companies, and the timing of those exits is uncertain. A secondary market for PE fund interests has developed, but selling a position typically involves a discount to net asset value and a lengthy transfer process. Investors must be prepared to have their capital locked for the full duration of the fund.

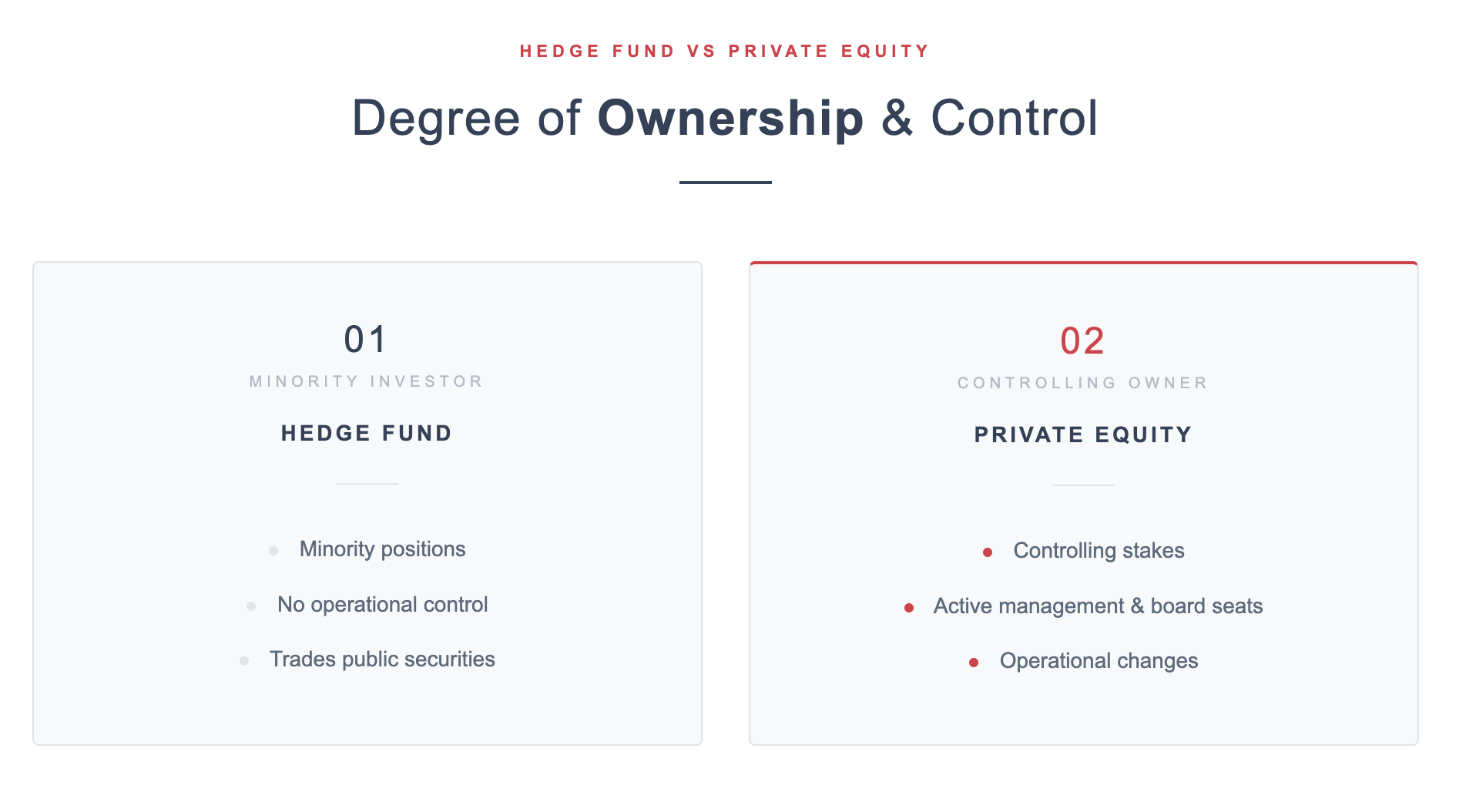

Hedge funds take minority positions in publicly traded securities. They typically hold small percentage stakes in companies and have no direct influence over management decisions or corporate strategy. Even activist hedge funds, which seek to influence company direction, rely on shareholder pressure rather than operational control.

Private equity firms acquire controlling or significant minority stakes in companies. This ownership position gives the GP board representation, decision-making authority over strategy, and the ability to directly implement operational changes. PE firms hire and replace management teams, restructure balance sheets, and drive strategic initiatives. This hands-on ownership is the primary mechanism through which PE creates value.

Hedge funds face market risk on a continuous basis. Their portfolios are marked to market daily, meaning returns are visible in real time and volatility is directly observable. The use of leverage and derivatives can amplify both gains and losses. However, many hedge fund strategies are specifically designed to manage and reduce risk through hedging, diversification, and active position management.

Private equity carries a different risk profile. Because portfolio companies are not publicly traded, their valuations are updated quarterly at best, which masks interim volatility. The real risks in PE are operational: a portfolio company may fail to execute its growth plan, market conditions may deteriorate, or an exit may be delayed. Leverage, which is used extensively in buyouts, amplifies both returns and losses. The illiquidity premium that PE investors expect compensates for this combination of operational risk and capital lock-up.

The sources of return for hedge funds and private equity differ fundamentally, reflecting their distinct approaches to value creation.

| Return Driver | Hedge Fund | Private Equity |

|---|---|---|

| Primary source | Trading alpha from security selection and timing | Operational value creation and strategic transformation |

| Leverage role | Amplifies trading returns; varies by strategy | Core component of buyout returns (LBO structure) |

| Market exposure | Variable; many strategies aim for low correlation | Correlated to private market valuations and exit conditions |

| Value creation mechanism | Identifying mispricings and market inefficiencies | Revenue growth, margin expansion, multiple expansion |

| Fee Component | Hedge Fund | Private Equity |

|---|---|---|

| Management fee | 1.0%–2.0% of AUM (industry avg. 1.50%) | 1.5%–2.0% of committed capital |

| Performance fee | 15%–20% of profits (industry avg. 19%) | 20% of profits (carried interest) |

| Fee basis | Charged on net asset value continuously | Management fee on committed capital; carry on realised gains |

| High-water mark | Standard; no performance fee until prior peak NAV is exceeded | Not applicable; carry calculated on fund-level returns |

| Preferred return (hurdle) | Less common; some funds use a hurdle rate | Standard 8% preferred return before GP earns carry |

Both vehicles follow variations of the “2 and 20” model, but the mechanics differ significantly. Hedge fund managers earn their performance fee on an ongoing basis as profits are generated, subject to high-water mark provisions. Private equity managers earn carried interest only after the fund has returned all invested capital plus the preferred return to LPs, aligning the GP's incentives with long-term value creation.

A critical distinction lies in the management fee basis. Hedge fund fees are charged on the current net asset value of the fund, meaning they fluctuate with performance. PE management fees are typically charged on committed capital during the investment period, regardless of how much capital has actually been deployed. This means PE investors pay fees on capital that may be sitting idle while awaiting deployment.

Every wealth journey starts with a conversation. Our advisers are ready to understand your objectives, assess your circumstances, and build a strategy tailored to your goals.

Begin Your Journey With Us| Metric | Hedge Fund | Private Equity |

|---|---|---|

| Target net return | 6%–12% annualised | 15%–25% net IRR |

| Return measure | Time-weighted return (TWR) | Internal rate of return (IRR) and MOIC |

| Volatility | Moderate; visible in daily/monthly NAV | Low reported volatility (smoothed by infrequent valuations) |

| Market correlation | Low to moderate (strategy-dependent) | Moderate to high (correlated with equity markets over full cycles) |

| Dispersion | Significant between top and bottom quartile | Very high; manager selection is critical |

According to HFR's 2025 Global Hedge Fund Industry Report, the hedge fund industry delivered strong aggregate returns in recent years, with total industry capital surpassing the $5 trillion milestone. However, returns vary dramatically by strategy, with top-quartile managers significantly outperforming the median.

Bain & Company's 2025 Global Private Equity Report highlights that PE has historically outperformed public markets over long horizons, though the magnitude of outperformance has compressed in recent years as more capital has entered the space. The report notes that buyout funds have delivered a median net IRR of approximately 14% over the past two decades, with top-quartile funds achieving significantly higher returns.

Many sophisticated portfolios include allocations to both hedge funds and private equity. Hedge funds can serve as a liquid diversifier and risk-management tool, while private equity provides long-term growth and an illiquidity premium. The optimal allocation depends on your liquidity needs, return objectives, time horizon, and overall wealth structure.

Both hedge funds and private equity carry risks that investors should carefully evaluate before committing capital. Understanding these risks is essential for setting realistic expectations and building a resilient portfolio.

This guide provides general information only and does not constitute financial advice. The comparison between hedge funds and private equity is intended for educational purposes. Individual circumstances, risk tolerance, and investment objectives should always be discussed with a qualified adviser before making investment decisions.

Hexagone Group — General Disclaimer.jpg)

The main difference lies in how each vehicle deploys capital. Hedge funds trade liquid securities across public markets using strategies such as long/short equity, global macro, and event-driven investing. Private equity funds acquire ownership stakes in private companies and create value through operational improvements over multi-year holding periods. This fundamental distinction drives all other differences in liquidity, time horizon, fees, and risk profiles.

Yes. Many sophisticated investors and institutions allocate to both vehicles as part of a diversified alternatives portfolio. Hedge funds provide liquidity, risk management, and non-correlated returns, while private equity offers long-term growth and an illiquidity premium. The optimal allocation depends on your liquidity needs, time horizon, and overall financial objectives. Contact our advisory team to discuss how both vehicles might fit within your portfolio.

Hedge fund minimums typically range from $100,000 to $5 million depending on the fund. Private equity commitments generally start at $250,000 for fund-of-funds structures and $5 million or more for direct fund access. Both vehicles require investors to meet accredited investor or qualified purchaser thresholds. Some platforms and advisory firms offer access at lower minimums through pooled structures or feeder funds.

Private equity has historically delivered higher absolute returns, with top-quartile buyout funds targeting 15%–25% net IRR. However, this comes with significant illiquidity and a capital lock-up of 7–12 years. Hedge funds target 6%–12% annualised returns with considerably more liquidity and lower volatility. Direct comparison is complicated by different return metrics (IRR vs TWR) and the illiquidity premium embedded in PE returns. The right choice depends on your specific objectives and constraints. Speak with our advisers to evaluate which return profile suits your situation.

Both hedge funds and private equity funds are regulated, though less extensively than mutual funds or other public investment vehicles. In the United States, both typically operate under SEC Regulation D exemptions, which limit their investor base to accredited investors and qualified purchasers. Fund managers must register as investment advisers and file disclosures including Form ADV and Form PF. The AIFMD provides a regulatory framework in Europe, while the DFSA regulates alternative funds in the DIFC. While lighter than public fund regulation, these frameworks provide meaningful investor protections and transparency requirements.