Hedge funds occupy a distinctive position within the alternative investment funds universe. Unlike traditional long-only strategies, they employ a broad toolkit — short selling, leverage, derivatives, and cross-asset trading — to pursue returns that are less dependent on the direction of public markets.

A hedge fund is a professionally managed investment pool that uses flexible strategies to generate returns in both rising and falling markets. The name “hedge” reflects the original concept of hedging market risk, though modern hedge funds pursue a far wider range of approaches and objectives.

A hedge fund is a pooled investment vehicle, typically structured as a limited partnership, that employs strategies beyond conventional long-only equity or bond investing. Hedge fund managers have broad discretion to invest across asset classes, use leverage, sell securities short, and trade derivatives — tools that are generally unavailable or restricted within traditional mutual funds.

The fund structure mirrors that of other alternative strategies:

| Structure | How It Works | Typical Use |

|---|---|---|

| Single fund | One vehicle, one strategy, one jurisdiction | Simpler strategies, single investor base |

| Master-feeder | Feeders collect capital, invest into a master fund | Accommodate onshore/offshore investors in one portfolio |

| Fund of funds | Invests across multiple hedge funds | Diversification across strategies and managers |

| Managed account | Investor's assets managed separately by the GP | Greater transparency, liquidity, and customisation |

Unlike public market funds that trade daily, hedge funds operate on defined subscription and redemption cycles. New investors subscribe at periodic intervals — typically monthly or quarterly — at the fund's most recently calculated NAV. Redemptions follow a similar schedule, subject to notice periods that commonly range from 30 to 90 days.

Hedge fund investors should understand several key liquidity constraints:

These terms exist because many hedge fund strategies involve positions that cannot be liquidated quickly without significant market impact.

Hedge funds employ a wide range of strategies, each with distinct return drivers, risk characteristics, and market exposures.

| Strategy | Description | Return Driver | Market Sensitivity |

|---|---|---|---|

| Long/Short Equity | Buy undervalued stocks, short overvalued ones | Stock selection (alpha) | Medium — net exposure varies |

| Global Macro | Trade across currencies, rates, commodities, equities based on macroeconomic views | Macro conviction + timing | Low to medium — directional bets |

| Event-Driven | Exploit corporate events: mergers, restructurings, spin-offs | Deal completion + catalyst timing | Medium — event-specific |

| Relative Value | Capture pricing inefficiencies between related instruments | Mean reversion + convergence | Low — market-neutral intent |

| Multi-Strategy | Allocate across several strategies within one fund | Diversification + tactical allocation | Low to medium — blended |

The most prevalent hedge fund strategy globally. Managers build a portfolio of long positions in companies they believe are undervalued and short positions in companies they consider overvalued. The “net exposure” — the difference between long and short allocations — determines how sensitive the portfolio is to broad market movements.

Global macro funds take directional positions based on macroeconomic analysis. These managers may trade currencies, interest rates, commodities, and equity indices, often using derivatives and leverage. Positions can shift rapidly as the macro outlook evolves.

Event-driven strategies focus on corporate catalysts: mergers and acquisitions, restructurings, bankruptcies, regulatory changes, and spin-offs. The manager's edge lies in analysing the probability and timing of specific events and their impact on security prices.

Relative value strategies seek to profit from pricing discrepancies between related instruments — for example, between a convertible bond and the underlying equity, or between two similar corporate bonds. These strategies typically aim to be market-neutral, generating returns from convergence rather than market direction.

Multi-strategy funds allocate capital across several approaches within a single vehicle, adjusting weights based on opportunity. This structure offers investors built-in diversification and allows the manager to deploy capital where opportunities are richest.

For investors exploring strategies with longer horizons and direct company ownership, private equity offers a complementary approach focused on operational value creation over multi-year holding periods.

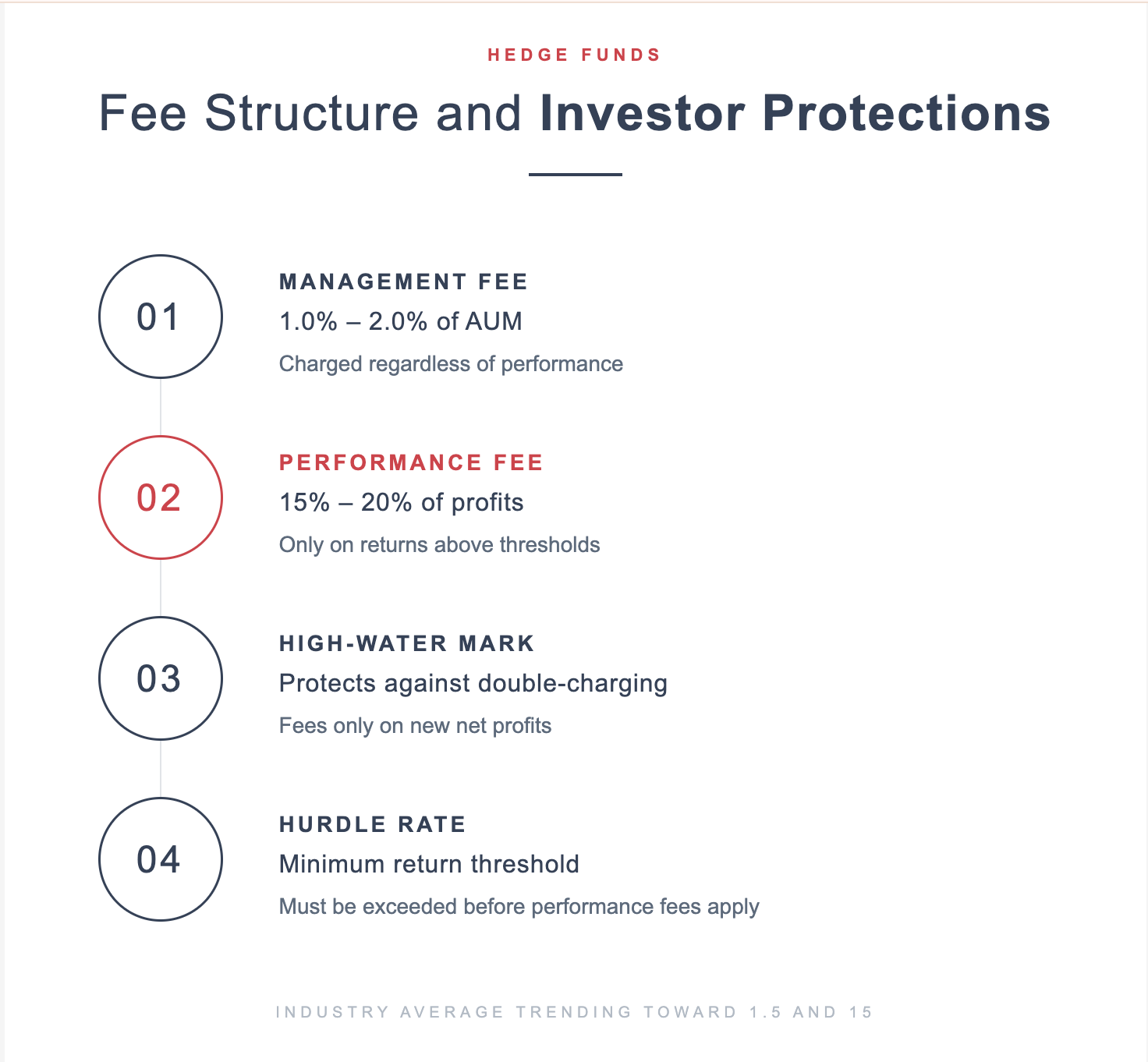

Hedge funds have traditionally operated on a “2 and 20” fee model, though industry evolution has introduced significant variation:

Average hedge fund fees have compressed over the past decade, with many institutional-grade funds now charging closer to “1.5 and 15” or offering tiered fee structures based on commitment size and lock-up duration.

Every wealth journey starts with a conversation. Our advisers are ready to understand your objectives, assess your circumstances, and build a strategy tailored to your goals.

Begin Your Journey With UsThe primary attraction of hedge funds within a broader portfolio is their potential to deliver returns with lower correlation to traditional equity and bond markets. This characteristic can improve portfolio diversification and reduce drawdowns during periods of market stress.

Key portfolio benefits include:

| Criterion | Hedge Funds | Private Equity | Private Credit |

|---|---|---|---|

| Liquidity | Monthly/quarterly (with lock-ups) | Illiquid — 7-12 year lock-up | Semi-liquid — 3-7 year terms |

| Return driver | Trading skill + market inefficiencies | Operational value creation | Yield premium + credit selection |

| Typical horizon | 1-3 years per position | 4-7 years per company | 3-5 years per loan |

| Leverage use | Common, varies by strategy | Primarily in LBOs | Moderate, varies by strategy |

| Correlation to equities | Low to moderate | Moderate (lagged) | Low |

Investors seeking income-oriented alternatives with regular yield may also consider private credit, which focuses on direct lending and non-bank debt strategies.

Given the wide performance dispersion across hedge fund managers, rigorous due diligence is essential. Key evaluation areas include:

Regulatory frameworks for hedge funds vary significantly across jurisdictions:

| Jurisdiction | Regulator | Key Framework |

|---|---|---|

| United States | SEC | Investment Advisers Act + Dodd-Frank |

| Europe | National regulators + ESMA | Alternative Investment Fund Managers Directive (AIFMD) |

| United Kingdom | FCA | UK AIFMD regime |

| DIFC (Dubai) | DFSA | Collective Investment Funds regime |

| Singapore | MAS | Securities and Futures Act |

| Global oversight | IOSCO, FSB | Cross-border coordination on leverage and systemic risk |

The Dubai International Financial Centre has established itself as a significant hub for hedge fund management and distribution in the Middle East. The DFSA's regulatory framework accommodates both Qualified Investor Funds and Exempt Funds, providing structures suitable for professional and institutional allocators.

GCC-based sovereign wealth funds and family offices have been active allocators to global hedge fund strategies, drawn by the diversification benefits and lower correlation to regional equity markets.

According to Preqin's 2025 Global Hedge Fund Report, Middle Eastern allocators have increased their hedge fund commitments notably over the past five years.

.jpg)

Investors considering hedge fund allocations should carefully evaluate the following risks:

For investors seeking exposure to alternative strategies through more defined payoff structures and capital protection features, structured products offer a different approach to accessing non-traditional return profiles.

This guide provides general information only and does not constitute financial advice. Individual circumstances, risk tolerance, and investment objectives should always be discussed with a qualified adviser.

A hedge fund is a professionally managed investment pool that uses flexible strategies — including short selling, leverage, and derivatives — to pursue returns in both rising and falling markets. Access is typically limited to qualified or institutional investors.

Investors can access hedge funds through direct fund subscriptions, fund of funds platforms, or managed account structures. Minimum investments vary widely, from $100,000 to $5 million or more. To explore options suited to your profile, begin your journey with us.

Returns vary significantly by strategy and manager. Diversified hedge fund indices have historically delivered mid-to-high single-digit annual returns with lower volatility than equities. Top-quartile managers may achieve considerably higher risk-adjusted performance.

Hedge funds are typically used as a portfolio diversifier rather than a core growth allocation. Their value lies in providing returns with lower correlation to traditional markets, reducing overall portfolio volatility. Contact us for more information about integrating hedge fund strategies into a broader wealth plan.

Key risks include leverage exposure, liquidity constraints (lock-ups and gates), manager performance dispersion, counterparty exposure, and limited transparency. Thorough due diligence on the manager, strategy, and operational infrastructure is essential.