Financial planning is one of the most important disciplines in personal finance - yet it remains one of the least understood. At its core, financial planning is the process of defining financial goals, assessing current resources, and building a structured strategy to achieve those goals over time. It is not a single event but an ongoing, adaptive process that evolves with your circumstances.

Whether you are just beginning your career, raising a family, approaching retirement, or managing significant wealth, a financial plan provides the clarity and discipline needed to make sound decisions.

Financial planning is the process of working out where you are financially, deciding where you want to be, and creating a plan to get there.

The CFP Board defines financial planning as “a collaborative process that helps maximise a client’s potential for meeting life goals through financial advice that integrates relevant elements of the client’s personal and financial circumstances.”

This definition captures two essential ideas:

Financial planning differs from simply managing money. Budgeting, saving, and investing are all components of financial planning - but the discipline brings them together into a coherent, goal-driven strategy. It answers the fundamental questions: What do I want to achieve? What resources do I have? What is the best path forward?

Importantly, financial planning is not only for the wealthy. The Financial Planning Standards Board (FPSB) - which oversees financial planning standards across 27 territories - emphasises that financial planning is relevant to individuals at every stage of life and income level. Whether the goal is building an emergency fund or structuring a multi-generational estate, the process applies equally.

The financial planning process follows a structured methodology recognised globally by the CFP Board and the FPSB. While the number of steps may vary slightly depending on the framework, the core logic is consistent.

According to the CFP Board’s 2024 Financial Planning Longitudinal Study, individuals who work with a financial planner report greater confidence in achieving their financial goals and higher levels of overall financial wellbeing.

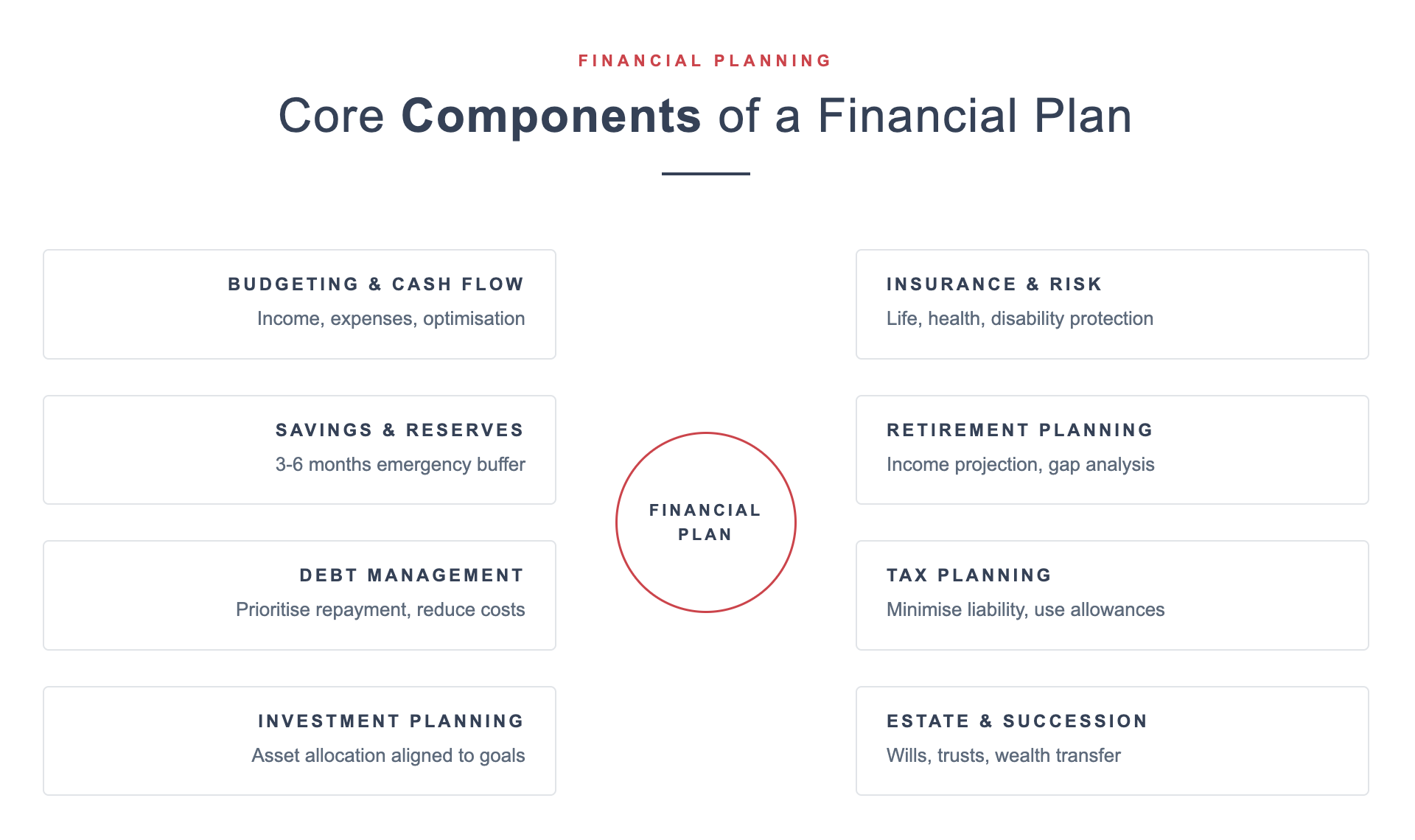

CFP Board — Financial Planning Longitudinal Study (2024)A comprehensive financial plan addresses multiple interconnected areas. No single component exists in isolation - each influences and is influenced by the others.

Every wealth journey starts with a conversation. Our advisers are ready to understand your objectives, assess your circumstances, and build a strategy tailored to your goals.

Begin Your Journey With UsThe benefits of financial planning extend well beyond investment returns. A well-structured financial plan provides clarity, confidence, and control over your financial life.

The OECD’s research consistently shows that individuals with higher financial literacy levels demonstrate better financial behaviours - including saving regularly, planning for retirement, and avoiding excessive debt. Financial planning is both a product of financial literacy and a driver of it.

While many aspects of financial planning can be managed independently, there are situations where professional guidance adds significant value.

When considering professional financial guidance, it is important to understand the distinction between financial planning and wealth management. For those whose needs extend beyond planning into active portfolio management, tax optimisation, and estate strategy, a financial planning and wealth management approach may be more appropriate.

In the DIFC, financial advisory services are regulated by the DFSA, which recorded 902 regulated entities in 2024 - a 14% year-on-year increase, with significant growth in the wealth management sector. Working with a regulated adviser ensures adherence to professional standards, transparency, and client protection.

Financial planning is not a theoretical exercise - it is a practical discipline that produces real, measurable outcomes when applied consistently.

In practice, an effective financial plan typically involves:

The most effective financial plans share common traits: they are realistic, flexible, well-documented, and regularly reviewed. They do not attempt to predict the future - instead, they prepare for multiple scenarios and create a framework for making sound decisions regardless of what unfolds.

This guide is provided for educational purposes only and does not constitute financial advice. Individuals should consult a qualified professional before making financial decisions.

Hexagone Group — General Disclaimer.jpg)

Financial planning is the process of setting financial goals, assessing your current situation, and creating a strategy to achieve those goals. It matters because it provides structure, discipline, and direction - helping individuals make informed decisions, prepare for the unexpected, and work toward long-term financial security.

The process typically involves six steps: understanding your current financial situation, defining goals, analysing the gap between current position and goals, developing recommendations, implementing the plan, and monitoring progress over time. Begin Your Journey With Us.

Financial planning is valuable at every income level. Even with modest resources, a plan can help you budget effectively, build emergency savings, manage debt, and start investing for the future. Professional guidance becomes especially valuable as financial complexity increases.

Most professionals recommend a comprehensive review at least once a year, with additional reviews triggered by major life events such as marriage, the birth of a child, career changes, or inheritance. Contact us for more information.

Investing is one component of financial planning, but financial planning is much broader. It encompasses budgeting, insurance, tax strategy, retirement planning, estate planning, and debt management - all integrated into a single, goal-driven strategy.