Structured products represent a distinct category within the alternative investment funds landscape, offering investors access to customised risk-return profiles that are not available through conventional instruments. Built by combining traditional securities with derivatives, they can be engineered to provide capital protection, enhanced yield, or leveraged market exposure.

A structured product is a pre-packaged investment that combines a bond with a derivative to create a specific payoff linked to the performance of an underlying asset — such as an equity index, a stock, an interest rate, or a commodity.

A structured product is a financial instrument whose return is linked to the performance of one or more underlying assets through the use of derivative components. Unlike a straightforward bond or equity investment, the payoff of a structured product is determined by pre-defined conditions set at issuance.

The key participants in a structured product are:

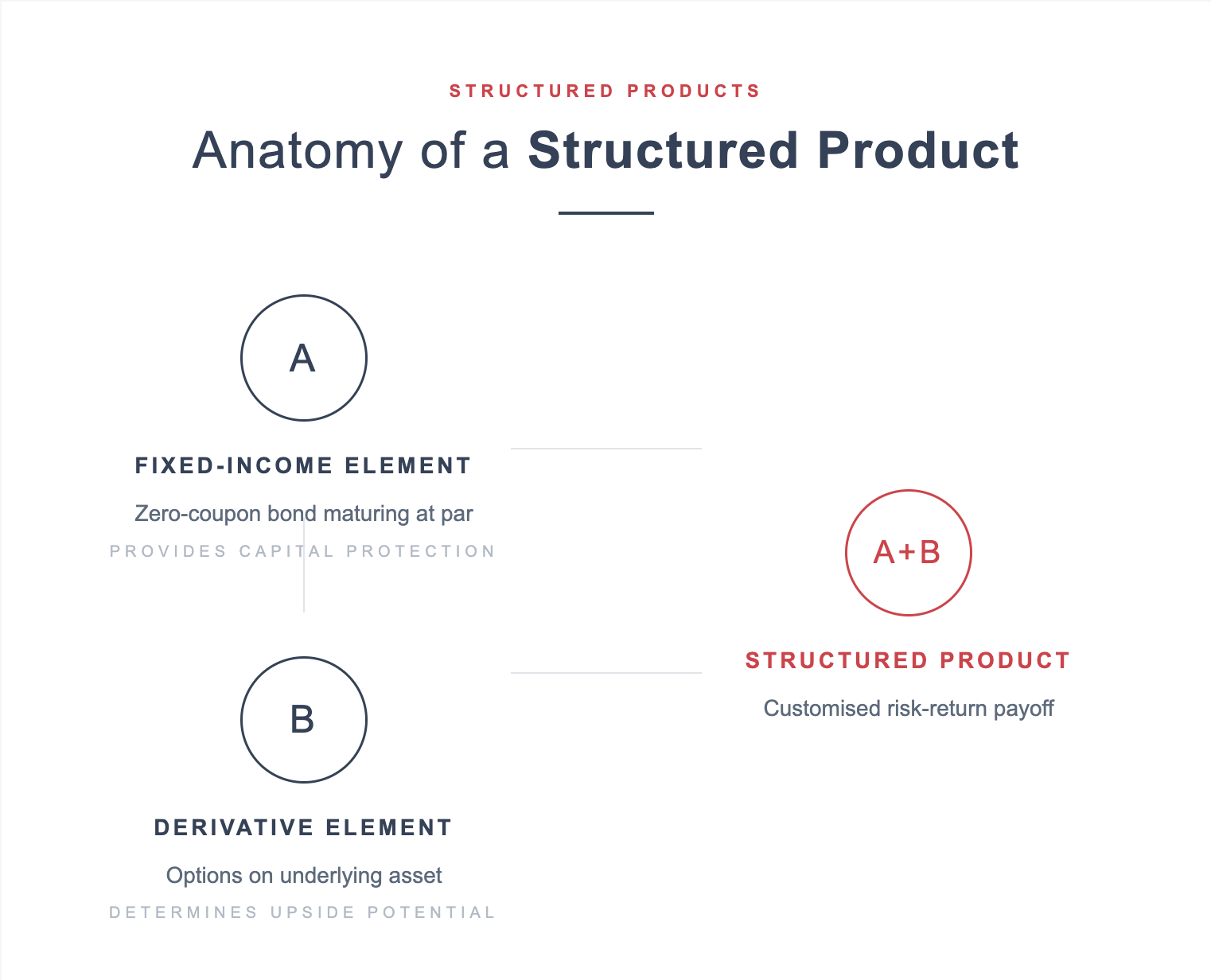

Every structured product is built from two fundamental components:

Consider a 3-year capital-protected note linked to the S&P 500 with 100% capital protection and 80% participation:

| S&P 500 Performance | Investor Receives | Effective Return |

|---|---|---|

| +30% | $100,000 + $24,000 = $124,000 | +24% |

| +10% | $100,000 + $8,000 = $108,000 | +8% |

| 0% | $100,000 | 0% (capital protected) |

| -20% | $100,000 | 0% (capital protected) |

The trade-off is clear: the investor gives up full participation in the upside (receiving 80% instead of 100%) and any dividends, in exchange for downside protection.

| Type | Payoff Logic | Typical Use Case | Risk Level |

|---|---|---|---|

| Capital-protected notes | 100% capital return + partial upside participation | Conservative investors seeking equity exposure with downside protection | Low to moderate |

| Yield enhancement (reverse convertibles) | Higher coupon in exchange for downside equity risk | Income-seeking investors willing to accept potential capital loss | Moderate to high |

| Participation / Tracker notes | Direct exposure to an underlying with possible leverage | Investors wanting targeted market exposure | Moderate |

| Autocallables | Automatic early redemption if underlying hits trigger levels, with coupon payments | Income generation with conditional capital protection | Moderate to high |

| Leveraged products | Amplified exposure (2x, 3x) to underlying moves | Sophisticated traders with short-term views | High |

The most conservative structure. At maturity, the investor receives at least the initial capital (subject to issuer credit risk), plus a percentage of any appreciation in the underlying asset. The protection comes at the cost of reduced participation and forgone dividends.

Including reverse convertibles, these offer above-market coupons in exchange for the investor bearing downside risk. If the underlying falls below a predefined barrier, the investor may receive shares or a reduced capital amount instead of full principal repayment.

The most popular structured product category globally. These products pay regular coupons and automatically redeem early if the underlying asset is at or above a specified level on predefined observation dates. If the product does not autocall, it continues to the next observation date. At final maturity, capital is typically protected unless the underlying has breached a barrier level.

Provide direct exposure to an underlying asset or basket, sometimes with leverage. They offer a way to access markets or themes that may be difficult to invest in directly.

The 2008 collapse of Lehman Brothers remains the most important cautionary tale in structured products. Investors who held capital-protected notes issued by Lehman discovered that “capital protection” depends entirely on the issuer's ability to pay. When Lehman filed for bankruptcy, note holders faced significant losses regardless of the product's payoff terms. This event underscores a fundamental principle: structured product investors must always assess issuer credit risk as carefully as the product's market risk.

Structured product investors must always assess issuer credit risk as carefully as the product's market risk.

Lehman Brothers collapse — September 2008

Every wealth journey starts with a conversation. Our advisers are ready to understand your objectives, assess your circumstances, and build a strategy tailored to your goals.

Begin Your Journey With UsUnlike traditional funds, structured product fees are not always transparent. Costs are typically embedded in the product's pricing rather than charged separately:

Before investing in any structured product, evaluate:

For investors considering other non-traditional strategies alongside structured products — such as direct lending and credit-focused approaches — private credit offers a complementary set of income-generating alternatives.

| Jurisdiction | Framework | Key Requirements |

|---|---|---|

| Europe (EU) | PRIIPs Regulation | Key Information Document (KID) mandatory for retail investors |

| United Kingdom | FCA Consumer Duty + PRIIPs | Suitability assessment, fair value, clear communications |

| United States | SEC / FINRA | Registration requirements, risk disclosure, suitability rules |

| DIFC (Dubai) | DFSA COB Module | Suitability, risk warnings, professional client classification |

| Global oversight | IOSCO | Thematic reviews on retail structured product regulation |

The DFSA's Conduct of Business (COB) module requires that structured products sold within the DIFC meet suitability standards and that investors receive clear risk disclosures. The DIFC framework aligns with international best practices while accommodating the region's specific market characteristics.

The global structured products market continues to expand, driven by several trends:

For investors interested in understanding how structured products fit alongside broader alternatives such as equity-based approaches, hedge fund strategies offer a different but complementary perspective on non-traditional market access.

.jpg)

Structured products are pre-packaged investments combining a bond with a derivative to create a customised payoff linked to an underlying asset. They can offer capital protection, enhanced income, or leveraged exposure depending on how they are designed.

Structured products are typically available through private banks, wealth managers, and financial advisers. Minimum investments range from $50,000 to $250,000 depending on the product and jurisdiction. To explore options suited to your profile, begin your journey with us.

No investment is without risk. Capital-protected products offer downside protection but depend on the issuer's credit quality. The 2008 Lehman Brothers collapse demonstrated that issuer default can override product-level protections. Thorough due diligence on both the product and the issuer is essential.

Structured products offer customised payoff profiles that bonds and ETFs cannot replicate — such as capital protection with equity upside. However, they are typically less liquid, more complex, and carry issuer credit risk. Contact us for more information about which approach best suits your investment objectives.

Key risks include issuer/counterparty credit risk, market risk (if barriers are breached), limited secondary market liquidity, embedded cost opacity, and complexity in understanding payoff mechanics. Investors should fully understand worst-case scenarios before committing capital.