Private equity represents one of the most significant segments within the alternative investment funds landscape. Over the past four decades, it has evolved from a niche strategy into a global asset class managing trillions of dollars across diverse sectors, geographies, and investment stages.

Capital invested in companies that do not trade on a public stock exchange. Unlike purchasing shares through a stock market, private equity investors commit capital to funds that take direct ownership stakes in businesses, often acquiring majority or full control.

The asset class operates through a fund structure built on two complementary roles:

| Criterion | Public Equity | Private Equity |

|---|---|---|

| Liquidity | Daily trading on open exchanges | Illiquid — capital locked for 7–12 years |

| Pricing | Continuous, market-driven | Periodic quarterly valuations by the GP |

| Regulatory oversight | Broad frameworks (SEC, FCA) | Fund-level governance through the LPA |

| Management approach | Passive, dispersed ownership | Active, hands-on operational involvement |

| Time horizon | Flexible, no minimum holding period | 7–12 year fund lifecycle |

| Return driver | Market appreciation + dividends | Operational improvement + leverage + repositioning |

This illiquidity is deliberate: it allows fund managers to pursue longer-term operational and strategic improvements without the pressure of quarterly earnings cycles.

The scope of private equity is broad. It encompasses everything from acquiring and transforming mature businesses through leveraged buyouts to funding early-stage ventures through venture capital. What unites these activities is the principle of active ownership — private equity managers do not simply hold shares; they seek to influence the direction, management, and operations of the companies in which they invest.

A typical private equity fund follows a lifecycle spanning ten to twelve years, divided into three sequential phases:

Private equity funds traditionally operate on a “2 and 20” fee model, though this has evolved considerably in recent years:

Private equity encompasses several distinct strategies, each with different risk-return characteristics, target companies, and value creation approaches.

| Strategy | Target Companies | Holding Period | Return Driver | Risk Profile |

|---|---|---|---|---|

| Leveraged Buyout (LBO) | Mature, cash-flow-positive businesses | 4–7 years | Operational improvement + financial leverage | Moderate |

| Growth Equity | Proven businesses needing capital to scale | 3–7 years | Revenue growth + margin expansion | Moderate-low |

| Venture Capital | Early-stage, innovation-driven companies | 5–10 years | Disruptive growth + market creation | High |

| Distressed / Special Situations | Financially challenged businesses | 2–5 years | Restructuring + discount to intrinsic value | High |

| Mezzanine | Mid-market firms needing flexible capital | 3–7 years | Current yield + equity upside (warrants) | Moderate |

| Secondaries | Existing LP commitments in PE funds | 3–5 years | Discount to NAV + reduced J-curve | Moderate-low |

Leveraged buyouts remain the largest segment of private equity by capital deployed. In an LBO, the fund acquires a company using a combination of equity and significant borrowed capital. The debt is typically serviced and repaid from the acquired company's cash flows, amplifying returns on the equity invested — though also amplifying risk if the business underperforms.

Growth equity occupies a middle ground between venture capital and buyouts. Funds invest in companies that have proven business models and revenue streams but need capital to scale further. These investments are generally minority stakes and involve less leverage than traditional buyouts.

Venture capital, while technically a subset of private equity, has developed into a distinct ecosystem. VC funds invest in early-stage companies, often in technology, healthcare, or other innovation-driven sectors. The risk-return profile is markedly different: most individual investments may fail, but successful outcomes can generate exceptional returns.

Distressed and special situations strategies target companies experiencing financial difficulty, operational challenges, or market dislocation. These investments require specialised expertise in restructuring, turnaround management, and often complex legal proceedings.

Secondaries involve purchasing existing LP commitments in private equity funds, typically at a discount to net asset value. This strategy provides liquidity to sellers and offers buyers access to diversified, mature portfolios with reduced J-curve exposure.

Investors interested in debt-based strategies that complement private equity — particularly mezzanine and distressed approaches — may also explore private credit, which focuses specifically on non-bank lending and direct lending structures.

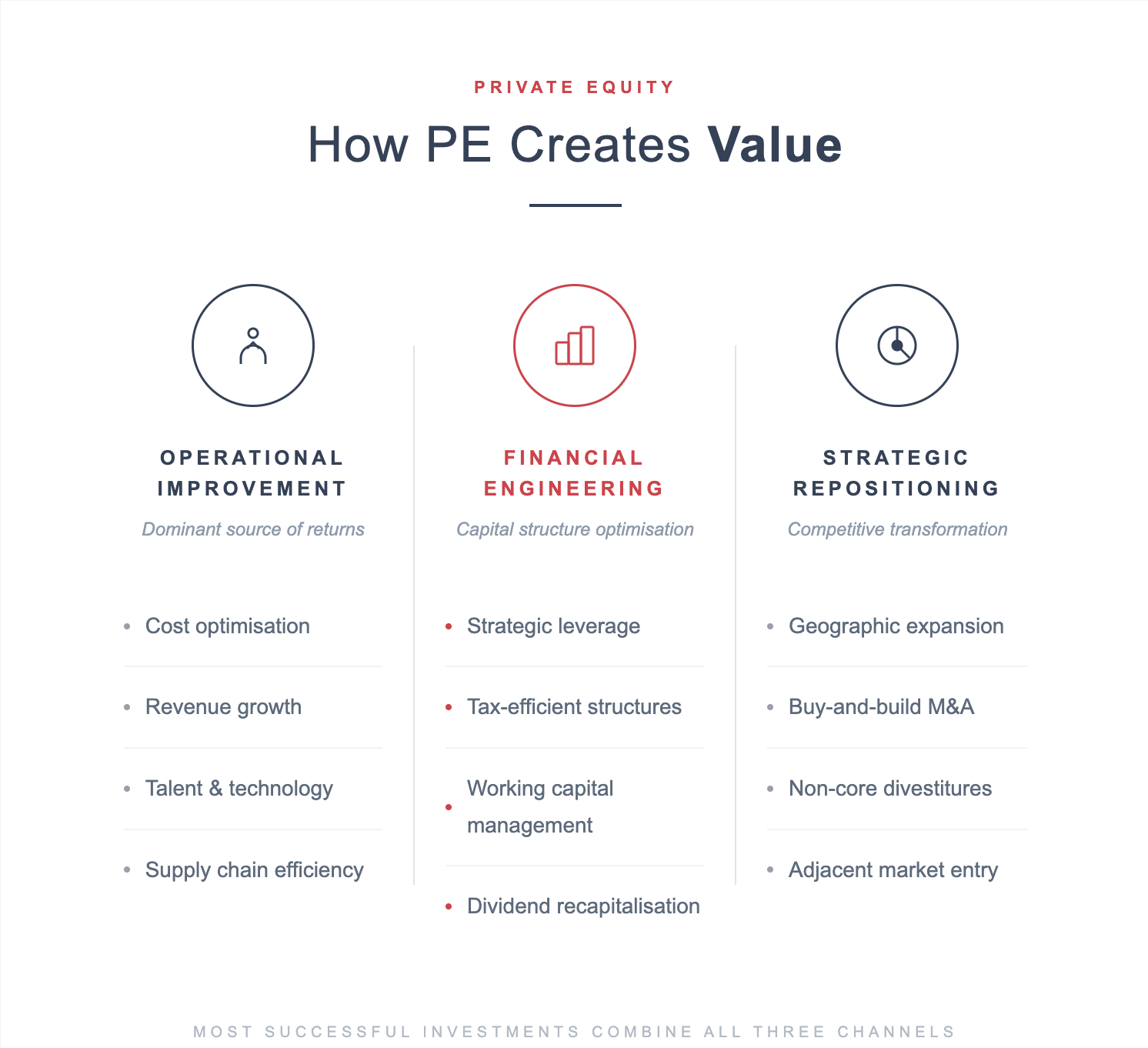

Private equity's fundamental premise is that active, concentrated ownership can unlock value that dispersed public ownership cannot. Value creation typically occurs through three interconnected channels:

Operational improvement has become the dominant source of returns as financial leverage has become less differentiated. The most successful private equity investments typically combine all three value creation channels.

McKinsey & Company — Global Private Markets Report (2025)A GP might acquire a business using moderate leverage, install a new management team, invest in technology to improve margins, and execute two or three add-on acquisitions to build market leadership — before selling the transformed business at a significant premium to the original purchase price.

Every wealth journey starts with a conversation. Our advisers are ready to understand your objectives, assess your circumstances, and build a strategy tailored to your goals.

Begin Your Journey With UsPrivate equity performance is measured using a distinct set of metrics:

| Metric | What It Measures | Key Consideration |

|---|---|---|

| IRR (Internal Rate of Return) | Annualised return accounting for timing of cash flows | Most cited metric, but sensitive to distribution timing |

| MOIC (Multiple on Invested Capital) | Total value returned / total capital invested | Simple and intuitive — 2.0x means double your money |

| TVPI (Total Value to Paid-In) | (Distributions + unrealised value) / capital called | Includes both realised and unrealised gains |

| DPI (Distributions to Paid-In) | Cash returned / capital called | Most conservative — only counts actual cash returned |

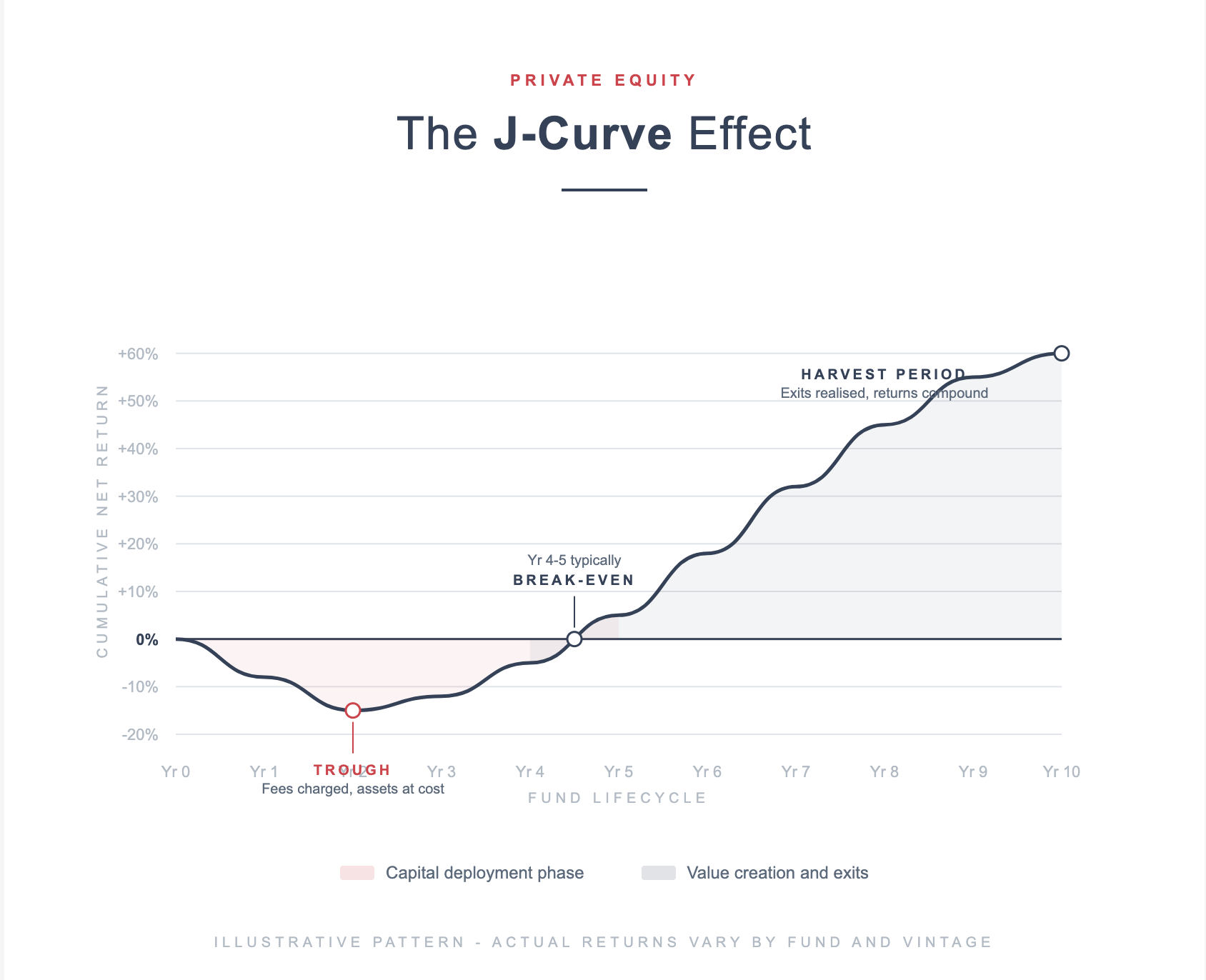

New PE fund investors should anticipate the J-curve — a characteristic return pattern in which the fund shows negative returns in its early years as management fees are charged and investments are marked at cost or below, before turning positive as portfolio companies mature and exits are realised. This pattern typically resolves over three to five years but requires investors to commit with a long-term horizon.

Historically, private equity has delivered a return premium over public equities, though the magnitude varies significantly by fund vintage, strategy, and manager quality. Top-quartile buyout funds have historically generated net IRRs in the mid-to-high teens, while median funds have delivered returns closer to low double digits.

However, several important caveats apply. Performance dispersion between top-quartile and bottom-quartile managers is considerably wider in private equity than in most public market strategies. Manager selection is therefore a critical determinant of investor outcomes. Additionally, past performance does not guarantee future results, and the return premium may narrow as more capital enters the asset class, increasing competition for deals and compressing entry valuations.

While private equity targets long-term value creation over several years, investors seeking strategies with shorter horizons and more frequent liquidity may also consider hedge fund strategies, which operate with fundamentally different return profiles and liquidity structures.

The largest allocators to private equity are institutional investors: pension funds, sovereign wealth funds, endowments, and insurance companies. These organisations typically have long investment horizons and the capacity to accept illiquidity in exchange for a potential return premium. Institutional allocations to private equity have grown steadily, with many large pension systems now targeting 10–20% of their total portfolio in private markets.

Historically, private equity was accessible primarily to institutional investors, with minimum commitments of $5 million to $25 million per fund. This landscape has shifted significantly. The emergence of feeder funds, semi-liquid private equity vehicles, and interval funds has broadened access for high-net-worth individuals and smaller family offices.

In Europe, the ELTIF 2.0 (European Long-Term Investment Fund) framework, updated in 2024, has created a regulated vehicle specifically designed to facilitate retail and semi-professional investor access to private markets, including private equity.

For investors seeking exposure to alternative strategies through more defined payoff profiles and tailored risk-return structures, structured products offer another approach within a diversified wealth strategy.

The Middle East, and particularly the Dubai International Financial Centre (DIFC), has become an increasingly significant hub for private equity activity. The DFSA's regulatory framework provides a robust governance environment for fund managers establishing operations in the region, with structures including Qualified Investor Funds (QIF) and Exempt Funds tailored to professional and institutional investors. GCC-based sovereign wealth funds and family offices have been among the most active allocators to global private equity strategies in recent years.

Private equity regulation varies significantly across jurisdictions:

| Jurisdiction | Regulatory Body | Framework |

|---|---|---|

| United States | SEC | Investment Advisers Act |

| Europe | National regulators + ESMA | Alternative Investment Fund Managers Directive (AIFMD) |

| DIFC (Dubai) | DFSA | Collective Investment Funds regime (QIF, Exempt Funds) |

| Global oversight | IOSCO, FSB | Focus on leverage, valuation practices, systemic risk |

The FSB's 2024 report on leverage in non-bank financial intermediation highlighted private equity as an area warranting continued regulatory attention across all jurisdictions.

Investors considering private equity should carefully evaluate several categories of risk before committing capital:

Investors considering private equity should be aware that this guide provides general information only and does not constitute financial advice. Individual circumstances, risk tolerance, and investment objectives should always be discussed with a qualified adviser.

.jpg)

Private equity involves pooling investor capital into funds that buy, improve, and sell companies not listed on public stock exchanges. Returns are generated through operational improvements and strategic growth over a typical holding period of four to seven years.

Investors can access private equity through traditional fund commitments, feeder funds, semi-liquid vehicles, and co-investment programmes. Minimum thresholds have decreased significantly in recent years. To explore options suited to your profile, begin your journey with us.

Top-quartile buyout funds have historically delivered net IRRs in the mid-to-high teens, though results vary widely by manager, vintage, and strategy. Past performance does not guarantee future outcomes, and manager selection is a critical determinant.

Private equity takes long-term ownership stakes in companies, typically holding for several years. Hedge funds generally trade more liquid instruments with shorter horizons. Both are alternative investments, but their risk-return profiles and liquidity characteristics differ considerably. Contact us for more information about how these strategies complement each other.

Key risks include illiquidity (capital locked for 7–12 years), leverage exposure, manager performance dispersion, valuation uncertainty, and blind pool risk. Thorough due diligence on fund managers and strategy alignment with personal objectives are essential.